Delta Neutral Strategy

A simulator for delta-neutral hedging strategies designed to reduce directional price exposure while highlighting funding, liquidation and execution risks.

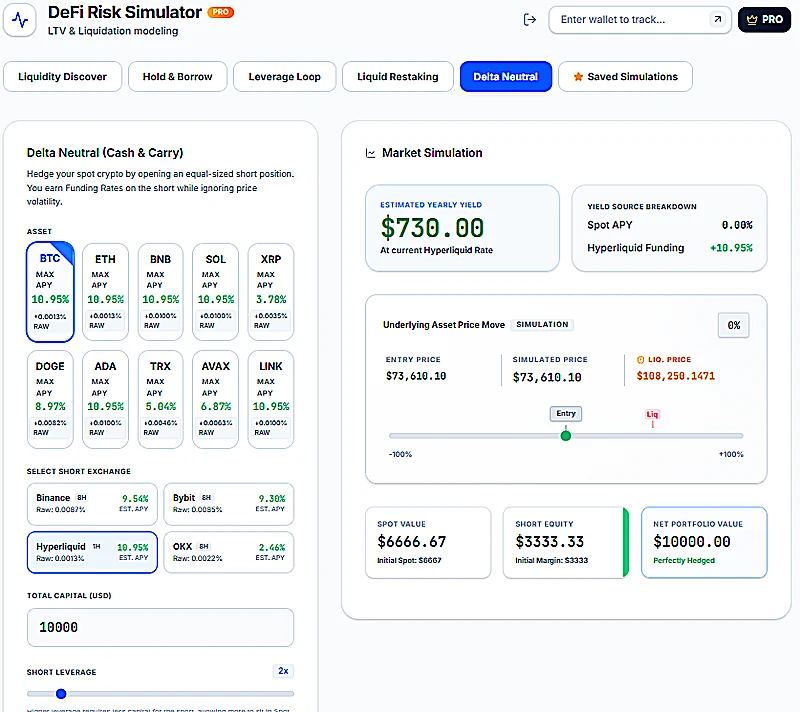

Hedge the position, not the headline

A delta-neutral strategy tries to reduce directional exposure by pairing a spot or LP position with an offsetting hedge, often through perpetual futures. The hedge can reduce price sensitivity, but it can also introduce funding cost, margin pressure, liquidation risk and rebalancing work.

This simulator helps you model spot, LP and short exposure together. It is built for scenario comparison: how the hedge behaves when price moves, funding changes, or margin becomes the main risk.

For the strategy logic behind hedge ratio, funding and short-side liquidation risk, read the delta-neutral hedge sizing and funding guide.

What this model helps you answer

Hedge size

How large should the short exposure be relative to the spot or LP exposure being modeled?

Funding

How much does the funding assumption help or hurt the position over the selected period?

Margin pressure

Can the short side survive a sharp move before the spot or LP side has time to offset it?

Residual risk

Where does the strategy still lose money after hedge cost, basis movement and execution assumptions are included?

Explore adjacent risk workflows

DeFi strategies usually connect more than one risk surface. These pages help you move from one assumption set to the next without reducing the app to a single calculator.

Start from LP exposure

If the hedge is for a concentrated LP, test the LP range and token exposure first.

Open the Concentrated Liquidity Simulator →Read the hedge guide

Review funding, basis, margin and short liquidation risk before treating a hedge as stable.

Read the delta-neutral guide →Compare vault exposure

If you are choosing between a hedge and vault allocation, compare drawdown assumptions too.

Open the Hyperliquid Vault Simulator →Stop guessing. Start optimizing.

Make data-driven DeFi decisions based on structured mathematical modeling. Explore liquidity ranges, hedging paths, and pool risk scenarios.