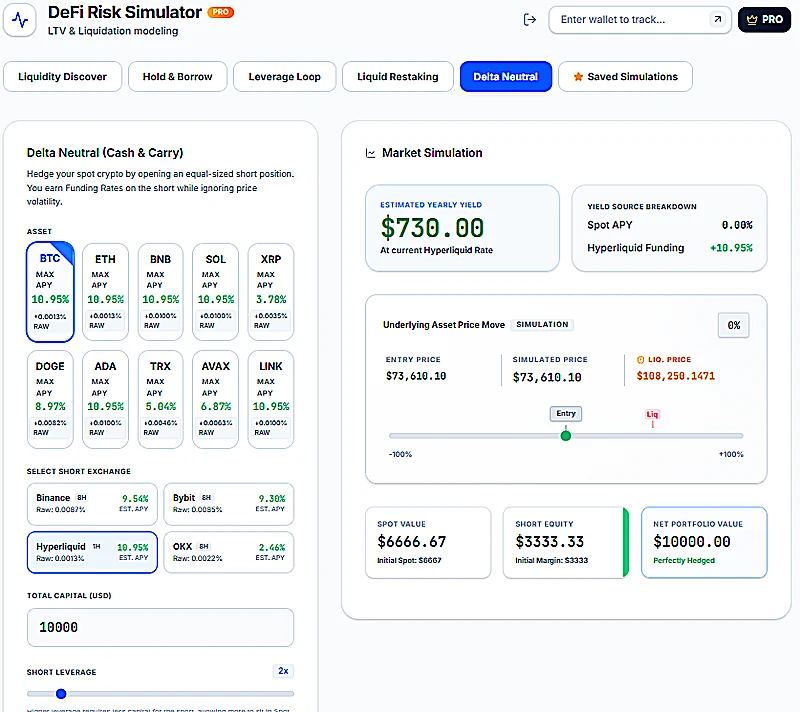

What Delta Neutral Means in Crypto

A delta-neutral strategy attempts to make the position less sensitive to the direction of the underlying asset. In crypto, this often means holding spot ETH or BTC and opening a short perpetual futures position. If the asset falls, the short may gain value. If the asset rises, the short may lose value.

The strategy can also apply to LP positions. A concentrated liquidity position often has changing exposure to the volatile token. A hedge tries to offset part of that exposure, but the exposure changes as price moves through the LP range.

The DeFiRiskSim Delta Neutral Strategy Simulator is designed to help users compare these assumptions before trading.

Funding Rate Is Not a Detail

Perpetual futures do not expire like traditional futures. They use funding payments to keep perp prices close to spot. If funding is positive, longs usually pay shorts. If funding is negative, shorts may pay longs. A delta-neutral strategy that depends on collecting funding can become unattractive when funding flips.

A simulator should let users test positive, neutral and negative funding environments. Without that, the strategy may look stable only because the model assumes favorable funding forever.

Hedge Size Is a Moving Target

A 100% hedge is not always correct. Spot exposure is simple, but LP exposure changes with price. A concentrated LP position can become more exposed to one token as the price moves. That means a hedge that is accurate at entry may be too large or too small later.

DeFiRiskSim models hedge strength as a scenario choice. Users can compare partial hedge, larger hedge and no-hedge outcomes. This is more honest than pretending there is one permanent hedge ratio.

The Hidden Risk: Short Liquidation

A short hedge can reduce downside exposure, but it introduces margin risk. If the underlying asset rallies, the short can lose money and approach liquidation. This can happen even while the spot or LP side gains value. The problem is timing and collateral management: gains on one side may not automatically protect margin on the other side.

That is why a good delta-neutral calculator should show margin buffer, effective leverage and short liquidation risk, not only net PnL.

A Practical Delta-Neutral Checklist

- Define the long exposure: spot, LP, vault or restaking position.

- Estimate current delta and how it may change.

- Choose hedge strength: partial, full or conservative.

- Model funding as positive, flat and negative.

- Check short liquidation price and margin buffer.

- Include trading cost, spread and slippage.

- Decide when the hedge should be rebalanced or closed.

FAQ

Is delta neutral risk-free?

No. It reduces one type of risk, but introduces funding, basis, execution, margin and liquidation risk.

Can I hedge a liquidity pool position?

Yes, but LP exposure changes as price moves. A static hedge can become too large or too small, so scenario modeling and rebalancing rules matter.

Why do funding rates matter?

Funding payments can be a source of yield or a cost. If funding flips against the hedge, the strategy can lose money even if price exposure is reduced.